Top Policies

No single policy can solve climate change, but a broad portfolio of policies already available to policymakers can drive down emissions. The most-effective policies in each countries may vary, but new modeling abilities highlight a small set of policies, aimed at specific segments of the economy, can achieve the deep decarbonization necessary to stay below the two-degrees Celsius target.

The power sector is responsible for 25% of annual global greenhouse gas emissions, produced when fossil fuels are burned to create electricity. Reducing power sector emissions is somewhat obvious: Use less coal, natural gas, and oil and replace them with zero-carbon resources. The most successful policies to achieve that goal have been renewable portfolio standards and feed-in-tariffs. However, complementary power sector policies accelerate this transition and allow the grid to run more nimbly. These policies can contribute at least 21% of the cumulative emissions reductions needed to meet the two-degree target.

The transportation sector contributes 15% of annual global emissions, dominated by petroleum consumption in cars, buses, and trucks. To reduce emissions, policymakers must reduce vehicle petroleum use through efficiency standards and vehicle and fuel fees, increase the number of alternative fuel vehicles (such as electric vehicles), and provide alternatives to owning and driving vehicles through better urban design. These policies can contribute at least 7% of the cumulative emissions reductions needed to reach the two-degree target.

Buildings are responsible for 8% of annual global emissions, and this is expected to significantly grow by 2050. Reducing these emissions requires improving the efficiency of building equipment such as air conditioning and heating equipment, improving the thermal efficiency of buildings, and improving the efficiency of appliances used in buildings. The most effective policies to accomplish this goal are building codes and appliance standards, which can contribute at least 5% of the cumulative emissions reductions needed to reach the two-degree target.

The biggest amount of emissions reductions come in the industrial sector, responsible for 38% of annual global emissions. Reducing industry sector emissions requires improving industrial production efficiency to lower energy demand and eliminating industrial process emissions. While industrial energy efficiency improvements can be achieved through energy efficiency standards, process emissions require a handful of tailored policy solutions. Together, they can contribute at least 26% of the cumulative emissions reductions needed to meet the two-degree Celsius target.

Cross-sector policies play a crucial complementary role in decarbonizing the global economy. One of the most important decarbonization policies, carbon pricing, typically operates across multiple sectors to help deliver large emission reductions. Similarly, research and development support is critical to lowering long-term decarbonization costs and typically targets technological advancement in different parts of the economy, helping reduce costs and increase savings from other policies.

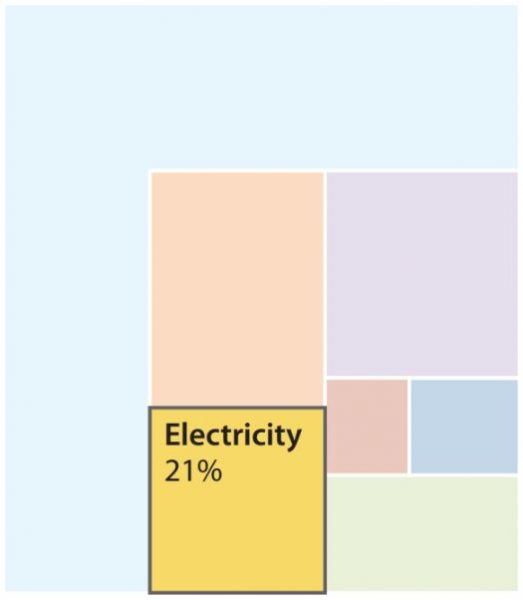

The Power Sector

Potential emissions reductions from the electricity sector.

The power sector is responsible for 25% of annual global greenhouse gas emissions today, with emissions of about 12 billion tons of CO2. Emissions are expected to grow to nearly 18.9 billion tons by 2050, comprising roughly 30% of annual greenhouse gas emissions in 2050. Without additional policies, the power sector will be responsible for 28% of cumulative emissions through 2050.

The growth in emissions is caused largely by growing amounts of coal and natural gas used for power generation. For example, the U.S. Energy Information Administration projects that global electricity generation from coal will grow from 8,100 terawatt-hours (TWh) in 2010 to 11,100 TWh in 2050, while global electricity generation from natural gas will grow from 4.6 TWh in 2010 to 11.1 TWh in 2050.

Reducing emissions from the power sector involves using lower- or zero-carbon technologies to produce power and reduce the demand for electricity. The best policies for increasing the share of carbon-free power generation are renewable portfolio standards and feed-in tariffs. Complementary power sector policies that encourage utilities to pursue cleaner options and to reduce the demand for electricity are also important, and other policies that seek to reduce demand by improving the efficiency of energy-consuming products (e.g., appliances) are tackled in other sections within the appropriate sector.

The power sector has an important role to play in helping decarbonize the economy. Together, the policies discussed in this section can contribute at least 21% of the reductions needed to meet the two-degree target.

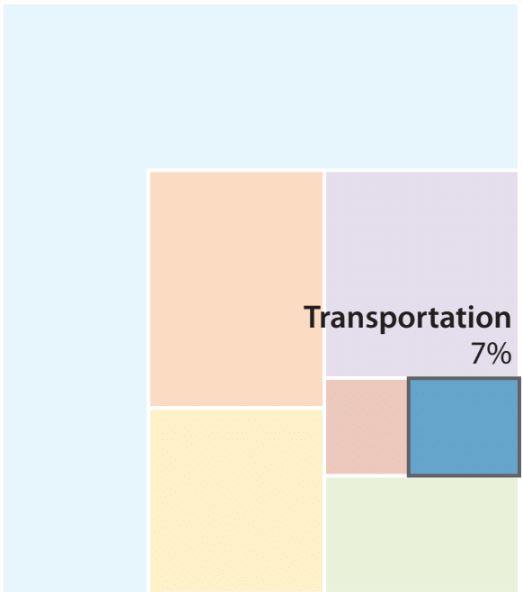

The Transportation Sector

Potential emissions reductions from transportation sector.

The transportation sector is responsible for more than 15% of annual global greenhouse gas emissions, with the most recent data showing CO2 emissions of about 7.5 billion tons in 2014. Emissions are expected to grow to more than 9 billion tons by 2050. Without additional policies, the transportation sector will be responsible for 14% of cumulative emissions through 2050.

The growth in emissions is largely due to increasing car ownership and freight transport. For example, passenger travel demand is expected to more than double between 2010 and 2050, and freight transport is expected to increase by nearly 60% over the same period. Without additional policy, the vast majority of this demand will be met with petroleum fuels, causing emissions to grow.

Reducing emissions from the transportation sector requires improving the efficiency of vehicles produced and the average efficiency of vehicles sold, increasing the share of electric vehicles sold, and providing alternatives to owning and driving a vehicle through smart urban planning.

Decarbonizing the transportation sector is an important element of any climate strategy, with significant co-benefits such as reduced particulate pollution and lost time due to traffic. Together, the transportation sector policies discussed here can contribute at least 7% of the reductions needed to meet the two-degree target.

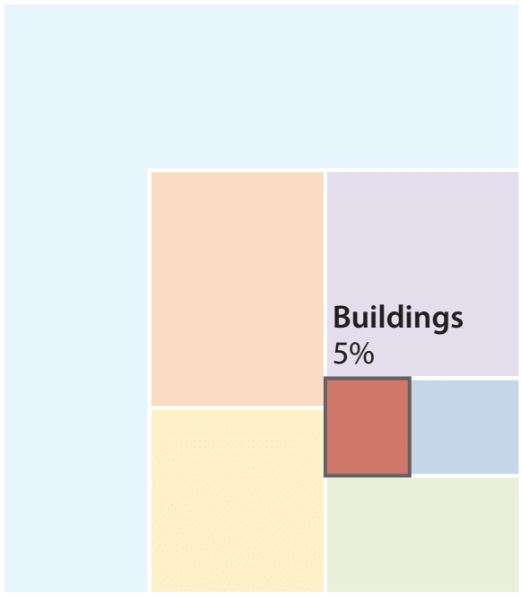

The Buildings Sector

Potential emissions reductions from building sector

The buildings sector is responsible for 8% of annual global greenhouse gas emissions today, with emissions of about 4 billion tons of CO2. Emissions are expected to grow to between 5 and 6 gigatons by 2050, and without additional policies the building sector will be responsible for 8% of cumulative emissions through 2050. Buildings and appliances are also significant drivers for electricity demand. For example, buildings are responsible for 54% of global electricity demand, and that share is expected to grow to nearly 60% by 2050. When electricity emissions attributable to the building sector are included, its share of today’s global greenhouse gas emissions increases to 20% and grows to 26% by 2050. The growth in emissions is due largely to a growing building stock filled with more energy-consuming technologies.

Reducing emissions from the building sector requires improving the efficiency of building equipment, such as air conditioning and heating equipment, the thermal efficiency of buildings, and the efficiency of appliances used in buildings. Decarbonizing the building sector and reducing demand for electricity are an essential part of lowering our overall carbon emissions. Building codes and appliance standards can achieve at least 5% of the reductions required by 2050 and an even higher share in later years, because higher efficiency standards take years to reach full effect.

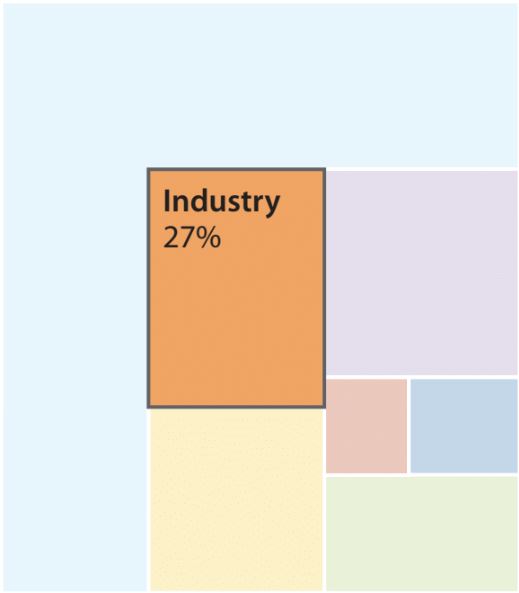

The Industry Sector

Potential emissions reductions from industry sector.

The industry sector, including agriculture and waste, is responsible for 38% of annual global greenhouse gas emissions today, with CO2e emissions of about 19 billion tons. Emissions are expected to grow to more than 42 billion tons by 2050. Without additional policies, the industry sector will be responsible for 49% of cumulative emissions through 2050. The industry sector is also a significant driver of electricity demand. For example, the industry sector is responsible for roughly 44% of global electricity demand, although that share is expected to fall to about 36% by 2050.

Industry sector emissions can be broken into two categories: emissions from fossil fuel combustion for energy use and process emissions. Process emissions are emissions released in industrial processes such as cement clinker manufacture and metallurgical coal coking. Additionally, we categorize non-energy emissions in agriculture and waste as process emissions. The share of industrial emissions from processes is significant. At least 10 billion tons of CO2e per year are from industrial processes: about 5.2 billion tons of CO2e per year from agriculture, 1.5 billion tons from waste, and 3.2 billion tons from more traditional manufacturing-related processes.

Reducing emissions from the industry sector therefore requires both improving the efficiency of industrial production, thus lowering demand for energy, and eliminating emissions from industrial processes. Heavily decarbonizing the industry sector is essential to hitting our climate targets. Improvements in industrial energy efficiency can achieve 16% of the necessary reductions by 2050, and reducing process emissions can achieve at least 10% of the necessary reductions.

Cross-Sector Policies

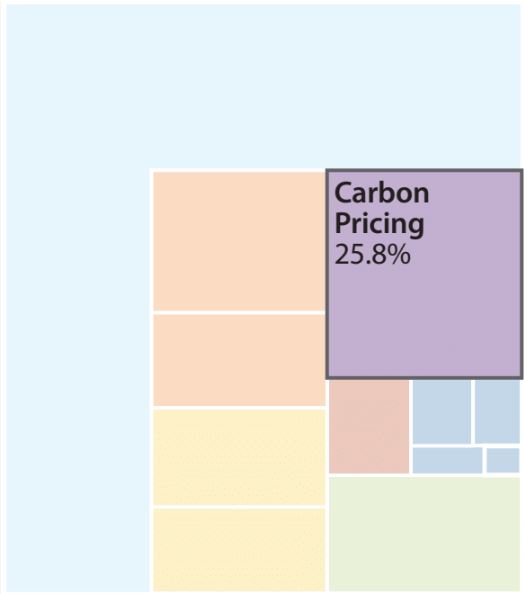

Potential emissions reductions from carbon pricing.

In addition to sector-specific policies, cross-sector policies are crucial to decarbonizing the economy. Indeed, one of the most important policies for decarbonization, carbon pricing, typically operates across multiple sectors, helping deliver large emission reductions. Similarly, support for research and development (R&D), which is critical to lowering the long-run costs of decarbonization, typically targets technological breakthroughs in different parts of the economy.

These policies are essential for decarbonizing the economy and doing so cost- effectively. Although the effect of carbon pricing is directly related to the price or emission cap used, in our analysis we find that strong carbon pricing set at the social cost of carbon can achieve 26% of the emission reductions necessary by 2050 to hit the two-degree target.

We do not explicitly model the effect of R&D on reducing emissions because of the challenges in making assumptions about R&D achievement and spending. However, R&D breakthroughs would lower the costs of meeting the two-degree target and would probably reduce the number and strength of policies needed. For example, decades of R&D, coupled with strong policies driving deployment, have helped drive down the costs of zero-carbon electricity generation technologies, including solar photovoltaics and wind turbines. As a result, it is much more cost-effective today to provide zero-carbon electricity than it has ever been in the past. The history of research-based cost declines coupled with well-designed policy shows how R&D fits together with other policy types to drive down costs and accelerate the clean energy transition.